The decision to move into a landed home is often framed as a lifestyle upgrade, but in the 2026 market, it’s actually a pivot into sovereign asset management. While your high-end condominium has served as a reliable vehicle for growth, upgrading from condo to landed property represents the final transition into a freehold legacy asset that offers unparalleled autonomy. However, with the Additional Buyer’s Stamp Duty (ABSD) for a second property now at 20% for Singapore Citizens, the margin for error in your execution has never been thinner.

You likely recognize that the path to a terrace or semi-detached home is fraught with logistical hurdles, from synchronizing your sell-buy timeline to managing the 55% Total Debt Servicing Ratio (TDSR) cap. This guide provides the strategic blueprint you need to master these financial and regulatory complexities with precision. We will examine how to leverage the current low interest rate environment, where fixed rates start from 1.35%, to secure your transition while preserving your long-term wealth and achieving true privacy.

Key Takeaways

- Establish your financial baseline by calculating net proceeds after CPF refunds and ensuring compliance with the 55% TDSR framework.

- Mitigate capital risks when upgrading from condo to landed by coordinating a precise sell-buy timeline that addresses ABSD obligations.

- Distinguish between property tiers, from terrace houses to Good Class Bungalows, to align your choice with a 30-year wealth preservation strategy.

- Prepare for the transition from managed facilities to full property autonomy, including an assessment of maintenance costs and future redevelopment potential.

- Gain a competitive advantage in the landed market by leveraging specialized expertise to identify undervalued assets and off-market listings.

Evaluating Your Financial Readiness for the Landed Leap

The successful execution of upgrading from condo to landed property hinges on a sophisticated capital architecture rather than simple income multiples. While your luxury condominium has likely appreciated, the actual liquidity available for your next acquisition depends on the precise calculation of your CPF refund plus accrued interest. This “hidden” cost often reduces the expected cash proceeds, potentially leaving a gap between your available funds and the required 25% downpayment. A deep understanding of Singapore’s housing landscape reveals a clear trajectory of asset progression, yet the transition to a terrace or semi-detached home remains the most complex financial maneuver an owner will undertake.

In the 2026 market, valuation gaps have become more frequent. Banks may value a property lower than the agreed purchase price, requiring you to cover the difference in cash. This “Cash Over Valuation” scenario makes substantial cash reserves a non-negotiable requirement for a seamless transition. Furthermore, while the current mortgage environment is favorable, with fixed rates starting from 1.35%, a conservative leverage strategy is essential. High-net-worth individuals often prioritize capital preservation over maximum leverage to ensure their legacy asset remains sustainable through shifting economic cycles.

Calculating Real Liquidity and the 25% Downpayment

Your acquisition strategy must account for the mandatory 5% cash downpayment and the remaining 20% which can be a mix of cash or CPF. Beyond the purchase price, you must budget for the Buyer’s Stamp Duty (BSD), which reaches 6% for the portion of the price exceeding S$3,000,000. It’s also prudent to maintain a “buffer fund” equivalent to 3% to 5% of the property value. Unlike condominiums, landed homes do not have a management corporation to handle structural repairs; you are the sole party responsible for the roof, external walls, and pest control from day one.

TDSR and LTV Limits: Navigating the 2026 Lending Landscape

The Total Debt Servicing Ratio (TDSR) remains a critical hurdle, capped at 55% of your gross monthly income. This limit includes all existing liabilities, such as car loans or credit lines, which can significantly compress your maximum loan quantum. As you age, the maximum loan tenure decreases, which sharply increases your monthly repayment obligations. To optimize these limits, some owners utilize “decoupling” strategies or part-share purchases. This allows one spouse to exit the current property ownership, enabling them to purchase the new landed home as a first-property owner, thereby avoiding the 20% ABSD and securing a full 75% Loan-to-Value (LTV) limit.

Deciphering the Landed Market: Tenure, Types, and Tiers

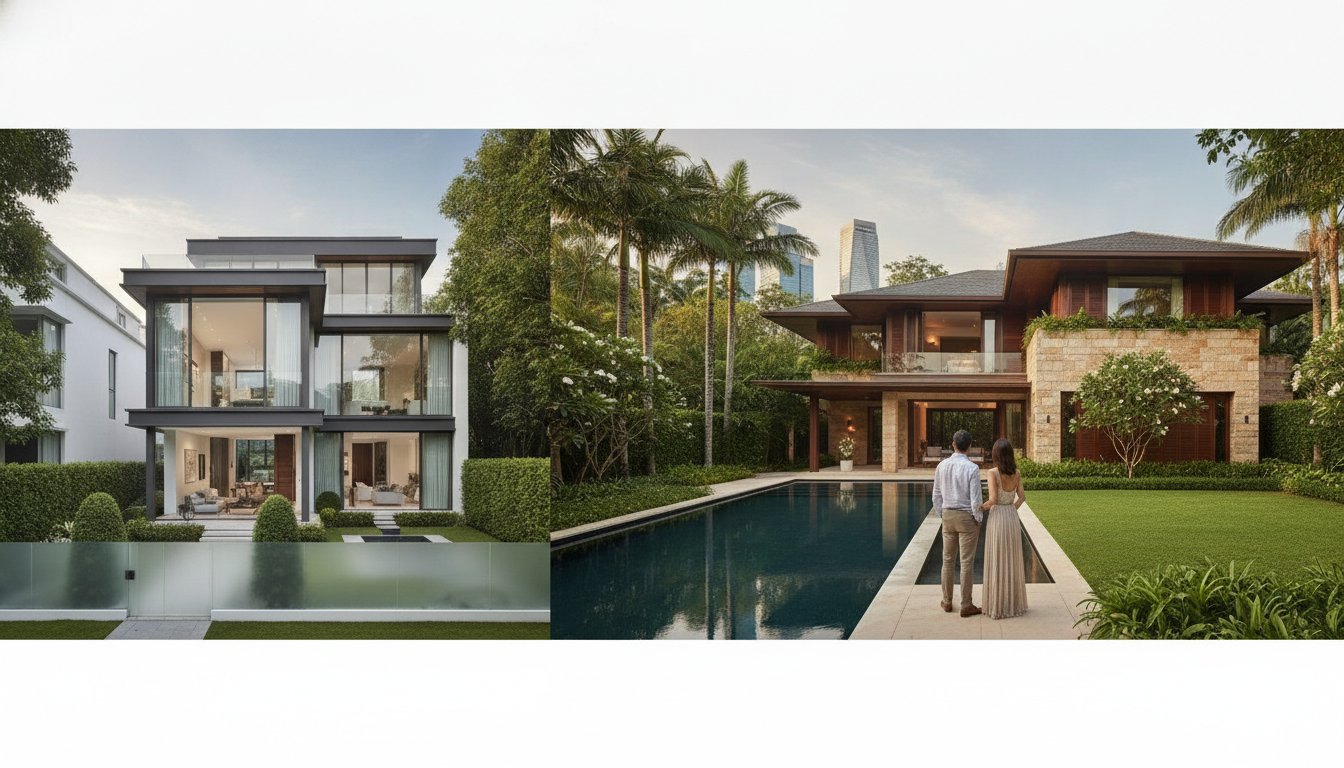

Success in upgrading from condo to landed property requires a fundamental shift in perspective. You’re no longer just purchasing floor area; you’re acquiring a portion of Singapore’s finite land mass. The market isn’t a monolith. It’s a structured hierarchy that ranges from terrace houses to the elite Good Class Bungalow (GCB) segment. Understanding where a property sits within this hierarchy is the first step in ensuring your capital is deployed effectively. While condominiums offer shared amenities, landed homes provide a level of autonomy that transforms your residence into a strategic financial asset.

Land size remains the primary driver of long-term capital appreciation. While a luxury condo’s price is often tied to its internal finishings and communal facilities, a landed property’s worth is anchored in its plot. Identifying undervalued assets often involves looking at older terrace houses in prime districts where the land-to-built-up ratio is high. These plots offer significant landed property redevelopment potential, allowing you to maximize the built-in area over time and create value that isn’t dependent on market sentiment alone. It’s about recognizing the intrinsic worth of the soil beneath the structure. For a deeper analysis of the regulatory and tax structures that govern these assets, the 2026 strategic wealth planning guide for investing in Singapore landed property provides a comprehensive framework for high-net-worth buyers.

The Scarcity Value of Freehold Landed Property

The debate between freehold and 99-year leasehold becomes clear when viewed through a 30-year wealth lens. Leasehold properties often provide higher rental yields initially, but they face terminal lease decay that can erode your equity. Freehold land remains the ultimate hedge against inflation and a cornerstone of legacy planning. It’s a permanent asset you can pass down through generations without the looming threat of a diminishing tenure. For those seeking to explore specific freehold opportunities, understanding the current price gap is essential to making an informed decision.

Matching House Type to Your Family’s Lifestyle Evolution

Your choice of house type should align with both your financial goals and your family’s growth. Each tier offers a different balance of privacy and land optimization:

- Terrace Houses: These serve as the ideal entry point. They offer the privacy of land without the daunting maintenance requirements of larger plots.

- Semi-Detached and Detached: These types offer increased autonomy. They’re suited for families who value side gardens, more natural light, and a greater distance from neighbors.

- Good Class Bungalows (GCB): This is the aspirational leap. GCBs represent the pinnacle of sovereign asset management, offering total privacy and the highest level of prestige in the Singapore market.

When you’re upgrading from condo to landed, it’s vital to remember that the GCB segment operates on entirely different liquidity and scarcity rules than standard bungalows. These assets are often held for decades, making them the most resilient property class during economic volatility. Choosing the right tier today ensures your home remains a source of both comfort and wealth for the next thirty years.

Synchronising the Transaction: The Sell-Buy Timeline

Precision in timing is the hallmark of a seasoned upgrader. When you’re transitioning between asset classes, the sequence of your transactions determines your cash flow liquidity and your exposure to tax liabilities. The most conservative route is the “Sell First, Buy Later” strategy. This path eliminates the need to pay the 20% upfront Additional Buyer’s Stamp Duty (ABSD) required for Singapore Citizens purchasing a second residential property. On a S$5 million terrace house, this saves you an immediate S$1 million cash outlay. It also provides absolute certainty regarding your budget, as you’ll have the net proceeds from your condominium sale firmly in hand before committing to a new purchase.

The “Buy First, Sell Later” approach is often preferred by those who refuse to compromise on their next home. In the landed segment, high-quality semi-detached or detached houses are rare; they don’t stay on the market long. Securing your dream home before selling your current one ensures you aren’t priced out during a search. However, this requires significant capital to cover the upfront ABSD and the 25% downpayment. Managing the transition period often involves negotiating an “extension of stay” with your condo buyer, which typically allows you to remain in your sold unit for up to three months while you finalize works on your new property.

Mastering the 6-Month ABSD Remission Window

For Singaporean married couples, the six-month ABSD remission window is a vital financial tool when upgrading from condo to landed. To qualify for a full refund of the 20% ABSD paid, you must sell your first residential property within six months of the purchase date of the landed home. This timeline is non-negotiable. Pitfalls often arise from delays in legal completion or a failure to find a buyer at your desired price point. Meticulous documentation and an aggressive marketing strategy for your condominium are essential to ensure the sale is finalized well within the IRAS-mandated timeframe.

Bridging Loans and Contingency Planning

Bridging loans serve as the financial connective tissue for this transition. These short-term facilities cover the downpayment gap until your condominium sale proceeds are released. With 2026 floating mortgage rates starting from 1.27% (3M SORA + 0.25%), the cost of capital is relatively low, but the exit strategy must be flawless. A successful strategist coordinates completion dates to facilitate a single-day move-in. If a gap persists, temporary leasing of a luxury apartment may be necessary. Always maintain a contingency fund to cover these interim housing costs and the interest on your bridging loan to avoid financial strain during the final stages of your asset progression.

Beyond the Purchase: Maintenance and Redevelopment Potential

Moving into a landed estate marks a definitive shift from passive facility management to active property stewardship. When you’re upgrading from condo to landed, you essentially become the CEO of your own private infrastructure. There’s no longer a Management Corporation Strata Title (MCST) to oversee common areas or structural repairs. This autonomy is liberating, yet it requires a disciplined approach to asset maintenance to ensure your property’s value continues to appreciate alongside the land it sits on.

Evaluating the structural integrity of an older terrace or semi-detached house is paramount before finalizing any purchase. You must distinguish between cosmetic flaws and systemic issues like foundation settlement or extensive termite damage. Many strategic investors look for properties with “good bones” where a targeted Additions & Alterations (A&A) project can significantly increase the built-up area without the prohibitive costs of a total rebuild. If the current structure is inefficiently placed on the plot, a full redevelopment may be the superior choice to maximize the land’s footprint and future resale value. Understanding how to evaluate and unlock landed property redevelopment potential in Singapore is essential to making the right call between an A&A project and a complete rebuild.

Budgeting for Landed Home Maintenance

Landed ownership introduces hidden operational costs that many condo dwellers overlook. Meticulous budgeting for roofing inspections, pest control, and external painting every five to seven years is essential. Garden and pool maintenance are not merely aesthetic choices; they’re non-negotiable for long-term value retention. You should establish a personal sinking fund, setting aside a monthly sum to cover these periodic capital expenditures. This proactive strategy prevents the accumulation of deferred maintenance, which can severely impact your property’s marketability when you eventually decide to exit. Successfully upgrading from condo to landed property requires a long-term view of these operational realities.

Identifying Redevelopment Gems

The URA Master Plan is your most valuable tool for identifying high-potential assets. By assessing the plot ratio and zoning regulations, you can identify “star buys” in areas slated for 3-storey zoning that currently only house 2-storey structures. This represents an immediate opportunity to increase your home’s internal square footage and total asset value. Working with a specialized architect allows you to refine the design to utilize every square meter of the permissible building envelope. If you’re ready to identify properties with untapped redevelopment potential, view our curated list of landed opportunities to begin your search.

Partnering with a Specialist for Your Asset Progression

The landed property market operates on a different set of fundamentals than the high-end condominium segment. While condo values are often influenced by project-wide transaction volumes and facility maintenance, landed assets are driven by land scarcity and specific plot characteristics. When you’re upgrading from condo to landed, you move from a standardized market to one where every asset is unique. This transition requires a partner who understands the intricacies of land titles, building setbacks, and the long-term wealth preservation potential of different landed tiers. It’s about moving beyond simple residential purchase into the realm of strategic land acquisition.

An Elite Strategist provides more than just access to listings. In the luxury market, particularly for detached houses and Good Class Bungalows (GCB), many of the most desirable properties never reach public portals. Sellers in this elite segment often prioritize privacy, choosing to transact through discreet, off-market channels. By partnering with a specialist, you gain entry into this exclusive network, ensuring you see the full spectrum of available inventory before it reaches the general public. This level of access is critical for securing a legacy asset that meets your specific requirements for privacy and autonomy.

The Value of Bespoke Brokerage in the Luxury Segment

Precision in negotiation is the cornerstone of a successful high-stakes transaction. A specialist broker employs sophisticated tactics designed to protect your interests while navigating the complexities of multi-million dollar sales. Whether you’re acquiring a terrace house as your first landed asset or transitioning toward a GCB, the process demands absolute transparency and integrity. We treat every transaction as a component of a larger, multi-generational property wealth plan. This ensures your acquisition today serves as a resilient foundation for your family’s future, preserving capital through market cycles while providing a superior lifestyle.

Your Next Steps Toward Landed Ownership

The journey toward a freehold legacy begins with a meticulous evaluation of your current holdings. We conduct a comprehensive portfolio review to determine the most strategic moment for your exit and entry. By mapping out a precise timeline, we ensure your transition is seamless, avoiding the common pitfalls of ABSD liabilities or temporary housing needs discussed earlier in this guide. If you’re ready to refine your strategy and secure your place in Singapore’s most exclusive residential segment, begin your asset progression journey with Vincent Lim. We provide the calculated competence and seasoned authority required to execute your move with total confidence.

Securing Your Legacy in the Singapore Landed Market

The transition from a high-end condominium to a landed estate is the ultimate realization of property ownership in Singapore. Successfully upgrading from condo to landed property in 2026 requires a surgical approach to financial planning and a deep understanding of land-based assets. You’ve seen how mastering the sell-buy timeline and identifying redevelopment potential can transform a residence into a resilient legacy asset for your family.

Executing this move with precision requires the guidance of a veteran who understands the nuances of the luxury segment. Vincent Lim, Executive Associate Director at OrangeTee & Tie, brings over 20 years of Singapore real estate expertise to your search. As a specialist in GCB and luxury landed sales, he provides the calculated competence and strategic insight necessary for high-stakes transactions. He ensures every detail, from ABSD remission to structural integrity, is managed with absolute transparency.

Consult with Vincent Lim on Your Landed Property Upgrade to begin mapping out your bespoke asset progression plan. Your future in a terrace, semi-detached, or detached home starts with a single, calculated step toward sovereign property ownership. We look forward to helping you secure your piece of Singapore’s finite land.

Frequently Asked Questions

Can I use my CPF to pay for a landed property purchase?

Yes, you can utilize your CPF Ordinary Account (OA) savings for the purchase of a landed property. You must first settle the mandatory 5% cash downpayment. The remaining 20% of the downpayment and subsequent monthly mortgage installments can be funded by CPF, provided the total amount stays within the Valuation Limit and the Withdrawal Limit set by the CPF Board.

How much cash is typically required for a S$5 million terrace house?

You generally need at least S$550,000 in liquid cash for a S$5 million terrace house transaction. This figure covers the 5% mandatory cash downpayment of S$250,000 and the Buyer’s Stamp Duty (BSD) of approximately S$289,600. It’s prudent to set aside additional cash for legal fees and a renovation buffer to manage the transition without financial strain.

What is the difference between A&A and a complete rebuild in Singapore?

Additions & Alterations (A&A) involve structural modifications that don’t increase the existing gross floor area by more than 50%. A complete rebuild requires demolishing the current structure to build a new one from the foundation. While rebuilding allows you to fully optimize the plot ratio and modernize the layout, A&A is a faster and more cost-effective way to enhance an older property.

Do I need to pay ABSD if I am upgrading from a condo to a landed home?

You’ll need to pay the upfront Additional Buyer’s Stamp Duty (ABSD) if the landed property is purchased before your condominium is sold. For Singapore Citizens, the rate for a second residential property is 20%. You can apply for an ABSD remission if you are a married couple and sell your first property within six months of the purchase date of the landed home.

Are landed properties harder to sell than luxury condominiums?

Landed properties typically have a longer transaction cycle because they cater to a more niche, high-net-worth buyer pool. While luxury condominiums benefit from higher liquidity and standardized pricing, landed homes are prized for their extreme scarcity. This scarcity ensures that landed assets remain highly resilient and maintain their value better during periods of market volatility.

What should I look for during a site inspection of an old landed house?

Prioritize the structural integrity of the building by checking for soil settlement, significant wall cracks, and roof leaks. When upgrading from condo to landed, you must also evaluate the condition of the electrical wiring and plumbing, as these are your sole responsibility. Investigating the neighborhood’s drainage and checking for signs of termite history is also essential for long-term peace of mind.

How does the URA Master Plan affect the value of my landed property?

The URA Master Plan determines the allowable building height and land use for your specific plot. If your area is rezoned from a 2-storey to a 3-storey semi-detached zone, your land’s intrinsic value increases due to its enhanced redevelopment potential. Understanding these zoning regulations allows you to identify properties with significant future capital appreciation built into the land.

Is it better to buy a 99-year leasehold landed or a freehold condo?

A freehold condo offers permanent tenure, but a 99-year leasehold landed property provides superior privacy and land autonomy. If your primary goal is upgrading from condo to landed for lifestyle expansion, a leasehold landed home can be a strategic entry point. However, for those focused on multi-generational wealth preservation, freehold land remains the most reliable hedge against inflation.