In the 2026 luxury real estate market, a 65 percent tax rate isn’t an impassable wall; it’s a strategic variable that separates the impulsive buyer from the elite legacy builder. You likely understand that acquiring a Good Class Bungalow or a detached house involves much more than just the listing price. The weight of significant tax outlays can feel like a strain on your liquidity, especially with recent regulatory shifts regarding trusts and residency status. It’s natural to worry that a miscalculation in your abds for landed property could compromise your broader acquisition strategy.

We’re here to ensure that doesn’t happen. This guide will empower you to master these complexities, allowing you to optimize your purchase while protecting your family’s long-term wealth. We’ll provide a clear roadmap of your 2026 tax liabilities, explain the nuances of strategic remissions for seniors and trusts, and give you the confidence to execute your next transaction with precision. From terrace houses to sprawling estates, your path to a secure legacy starts with a calculated and methodical approach to tax.

Key Takeaways

- Understand how the 2026 regulatory framework distinguishes landed property from other residential assets to prioritize market stability and long-term value.

- Identify your precise tax bracket by evaluating residency status and property counts to accurately project the abds for landed property.

- Master the calculation of total acquisition costs; this includes the integration of Buyer’s Stamp Duty and legal fees for a comprehensive financial overview.

- Explore the strategic use of living trusts and decoupling to navigate the 65 percent upfront tax requirements and protect your family’s liquidity.

- Learn to integrate tax optimization into a 10-year asset progression roadmap to ensure your acquisition aligns with long-term wealth preservation.

What is ABSD for Landed Property in 2026?

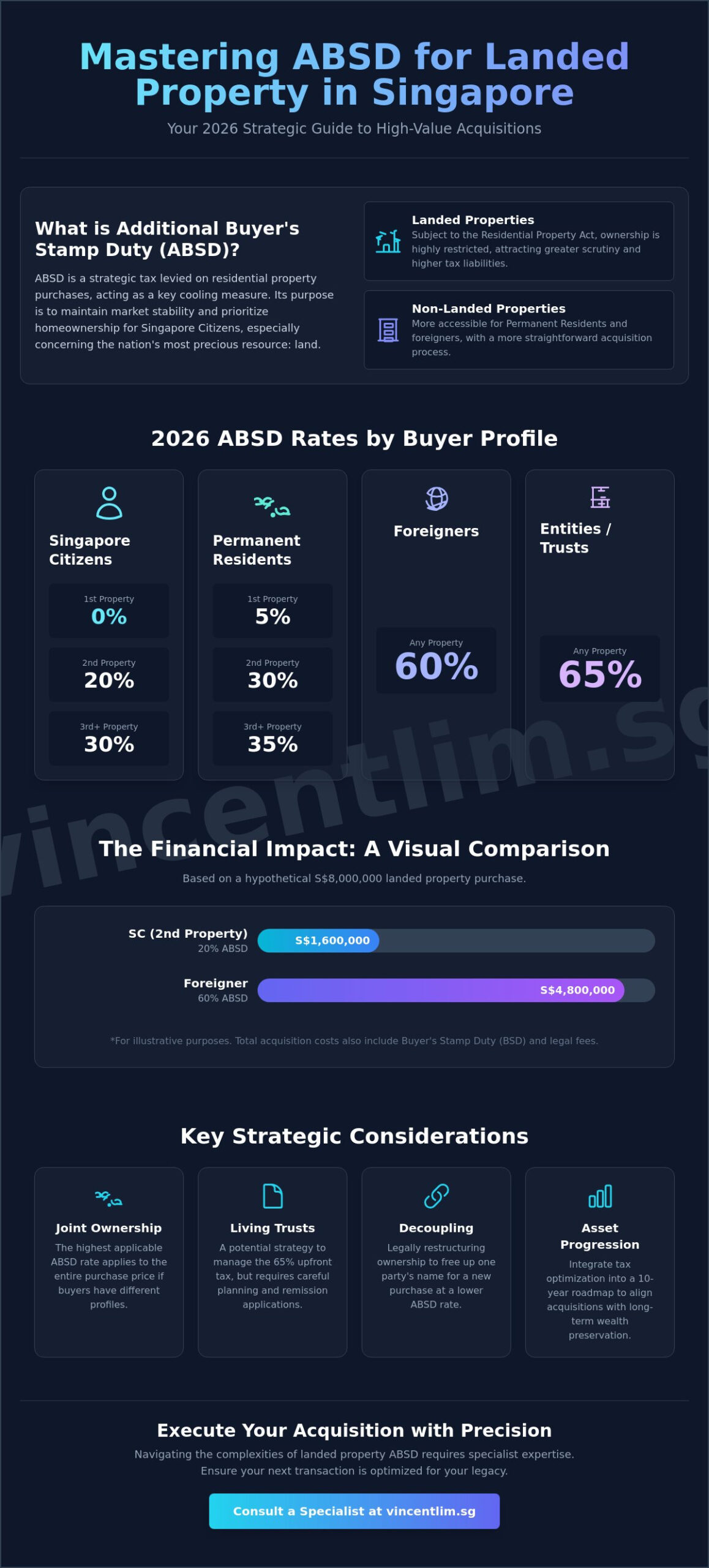

Additional Buyer’s Stamp Duty (ABSD) functions as a strategic tax levied on residential purchases in addition to the standard Stamp Duty in Singapore. It serves as a primary cooling measure designed to ensure residential stability and prioritize homeownership for Singapore Citizens. For many sophisticated investors, the search for “abds for landed property” isn’t merely a tax inquiry; it’s a quest for financial clarity before committing to a legacy asset. In 2026, these rates remain a critical component of the acquisition process, reflecting the government’s stance on managing capital inflows into the domestic housing market.

Landed properties attract a level of scrutiny that luxury condominiums do not. Because land is Singapore’s most precious resource, the government treats the acquisition of terrace houses, semi-detached houses, and detached houses with exceptional care. This scrutiny ensures that the limited supply of landed homes serves the national interest. Consequently, the tax implications for these assets are often the most significant part of an acquisition’s closing costs, requiring a calculated and methodical approach to planning.

The Evolution of Cooling Measures

The history of Singapore’s property market is defined by proactive intervention. Rates have seen progressive hikes, most notably the sharp increases implemented on April 27, 2023, which set the tone for the current 2026 landscape. These adjustments weren’t reactive; they were strategic moves to decouple residential prices from global liquidity. Today, the rates reflect a commitment to sustainable growth rather than volatile speculation. In the 2026 landed segment, ABSD is defined as a profile-based fiscal instrument designed to regulate the velocity of high-value land transfers.

Landed vs. Non-Landed: Tax Distinctions

Acquiring a landed asset involves navigating the Residential Property Act, which restricts ownership to Singapore Citizens with few exceptions. This legal framework creates a distinct barrier to entry that non-landed assets lack. While a luxury condominium might be a straightforward purchase for a Permanent Resident, a Good Class Bungalow (GCB) requires a much more rigorous approval process from the Land Dealings Approval Unit.

The property type directly influences your total liability. Because landed homes typically sit at higher price points, the 20% or 30% ABSD rates for second or third properties result in substantial cash requirements. For instance, a detached house purchase by a Singapore Citizen owning their second home now requires a 20 percent upfront ABSD payment. This highlights why understanding the nuances of abds for landed property is vital for any serious buyer. The stakes are higher, the regulations are tighter, and the need for a precise acquisition strategy is absolute.

Determining Your Liability: Residency and Property Count

Your financial liability in a landed property acquisition is governed by two primary factors: your residency status and the number of residential properties you currently own. In the 2026 market, the Inland Revenue Authority of Singapore (IRAS) maintains a strict hierarchy that prioritizes domestic homeownership. Before you begin evaluating a terrace house for sale singapore, it’s essential to audit your global and local property portfolio. The “count” includes any residential interest held, even if it’s a partial share or held through a trust that hasn’t been properly remitted.

Joint ownership requires particular caution. If multiple buyers with different residency profiles or property counts purchase a home together, the highest applicable rate applies to the entire purchase price. For example, if a Singapore Citizen purchasing their first home partners with a foreigner, the 60 percent foreigner rate is levied on the full valuation. This alignment with Singapore’s Property Tax Policy ensures that cooling measures aren’t bypassed through structured partnerships. Understanding these mechanics is the first step in calculating the total abds for landed property.

Singapore Citizens and Permanent Residents

Singapore Citizens (SC) enjoy the most favorable tax treatment, with a 0 percent rate on their first residential property. However, the liability rises to 20 percent for a second property and 30 percent for any subsequent acquisitions. Singapore Permanent Residents (SPR) face a different trajectory. They pay 5 percent on their first home, but this jumps significantly to 30 percent for a second property and 35 percent for a third. For families managing multiple assets, it’s often more efficient to consolidate holdings before pursuing a high-value landed estate.

Foreigner and Entity Acquisitions

Foreign investors face the most significant barrier with a flat 60 percent ABSD rate on any residential purchase. Entities and trusts are subject to an even higher rate of 65 percent. It’s worth noting that citizens from specific countries with Free Trade Agreements (FTAs), such as the United States, Iceland, and Switzerland, may be eligible for the same tax treatment as Singapore Citizens. If you fall into these categories, the savings on a detached house or GCB can be substantial. For a comprehensive understanding of the eligibility criteria, approval processes, and strategic pathways available to non-citizens, the detailed breakdown of how foreigners can buy landed property in Singapore provides essential guidance on navigating these complex regulatory frameworks. For those navigating these high-stakes entries, partnering with a seasoned strategist can help clarify these regulatory nuances before you commit capital.

Quantifying the Financial Impact on Landed Assets

Precision is paramount when calculating the total cost of a high-value acquisition. The Inland Revenue Authority of Singapore (IRAS) determines your tax liability based on the higher of the actual purchase price or the professional market valuation. This “higher of” rule ensures that transactions reflect current market realities, leaving no room for artificial price suppression to reduce tax exposure. When you prepare for an acquisition, your financial roadmap must account for the Buyer’s Stamp Duty (BSD), the abds for landed property, and associated legal fees as immediate cash requirements.

Consider the financial breakdown for a $10 million detached house for sale singapore. For a Singapore Citizen acquiring this as their second residential property, the 20 percent ABSD rate translates to a $2 million cash outlay. When combined with the tiered BSD rates, which reach 6 percent for amounts exceeding $3 million, the total tax liability surpasses $2.5 million. This entire sum must typically be settled within 14 days of exercising the Option to Purchase (OTP). Failure to secure this liquidity within the narrow window can jeopardize the transaction and lead to significant late payment penalties.

You should consult the Official ABSD rates and regulations to ensure your calculations align with the most recent 2026 mandates. Managing these outlays requires a sophisticated approach to capital allocation, especially when dealing with the highest tiers of the market. A disciplined understanding of your landed property downpayment in Singapore — including how to structure the initial 5% cash and 20% CPF components alongside your ABSD obligations — is essential for ensuring your liquidity remains intact throughout the transaction.

The GCB Premium: High-Value Calculations

In the Good Class Bungalow (GCB) segment, the numbers escalate rapidly. A $30 million GCB purchase by an investor on their third property triggers a 30 percent ABSD, amounting to a $9 million tax obligation. A mere 1 percent discrepancy in a $30 million valuation results in a $300,000 variance in taxable value, potentially triggering immediate scrutiny or under-stamping penalties. Meticulous valuation is not just a preference; it’s a requirement for regulatory compliance.

Stamp Duty for Mixed-Use Landed Assets

Strategic buyers often encounter shophouses or properties with ‘Part-Residential’ land designations. These assets require a calculated apportionment of value. Only the residential component attracts ABSD, while the commercial portion remains exempt. Navigating these complexities involves coordinating with professional valuers to justify the price breakdown to IRAS. Proper apportionment can significantly improve your tax efficiency without compromising the integrity of your acquisition strategy.

Strategic Mitigation: Trusts, Decoupling, and Remissions

Sophisticated asset management requires more than just capital; it demands a mastery of regulatory remissions. For many families, the ‘Decoupling’ strategy remains a cornerstone of portfolio expansion. By legally transferring a share of an existing property to a spouse, one individual can regain ‘first-time buyer’ status. This move effectively reduces the abds for landed property from 20 percent to 0 percent for the subsequent purchase. It’s a precise maneuver that requires careful coordination with legal counsel to ensure compliance with the latest 2026 frameworks.

Couples looking to upgrade also benefit from matrimonial remissions. If a Singapore Citizen couple acquires a second residential property, they must pay the ABSD upfront. However, they can apply for a full refund if they sell their first property within six months of the second property’s purchase date. This mechanism provides a vital liquidity bridge for those transitioning from a luxury condominium to a more substantial estate. When choosing such an asset, the distinction between freehold vs leasehold landed property becomes a critical tax planning factor. High tax outlays are more easily justified when the underlying asset offers perpetual ownership and generational value.

Navigating the ABSD (Trust) Framework

As of April 27, 2023, any transfer of residential property into a living trust triggers a 65 percent ABSD rate. This upfront cost is significant, yet remissions are possible if the trust meets specific criteria. The beneficiaries must be identifiable individuals, and the property must vest in them immediately. Applying for this refund requires a submission to IRAS within six months of the instrument’s execution. In 2026, using trusts is less about immediate tax avoidance and more about disciplined legacy planning and asset protection for the next generation.

FTA Remissions for Foreign Investors

Certain foreign nationals enjoy a unique advantage under Free Trade Agreements. Citizens and Permanent Residents of Iceland, Liechtenstein, Norway, and Switzerland, as well as United States Citizens, are eligible for the same ABSD treatment as Singapore Citizens. This means a first-time buyer from these nations pays 0 percent ABSD rather than the standard 60 percent. If you believe your profile qualifies for these specific exemptions, consulting with an elite strategist is the most efficient way to validate your eligibility and refine your acquisition timeline.

Strategic Asset Progression: The Specialist’s Perspective

Elite wealth management requires a proactive stance. You shouldn’t wait until you’ve found a detached house to calculate your stamp duty liability. Instead, your tax profile should define the very assets you target. Successful acquisition begins long before the first viewing. By integrating tax planning into the initial phase of your journey, you eliminate the risk of miscalculating total acquisition costs and ensure your liquidity remains intact for future opportunities. Precision is the foundation of peace of mind.

A 10-year asset progression roadmap is the hallmark of a seasoned investor. This long-term view allows you to absorb the abds for landed property as a strategic investment in land scarcity. When you view tax as a component of the total cost basis rather than an isolated penalty, you can focus on the long-term capital appreciation that only Singapore’s limited landed supply can provide. An elite strategist identifies opportunities where the intrinsic value of the land outweighs the entry friction, ensuring that your capital works effectively from the moment of purchase.

Maximizing ROI Despite High Entry Costs

Landed property remains the undisputed pinnacle of the real estate pyramid. While entry costs in 2026 are higher than in previous decades, the scarcity of Good Class Bungalows and semi-detached houses creates a natural hedge against inflation. Strategic land acquisition is less about immediate rental yield and more about the preservation of a family legacy. The upfront tax is a trade-off for owning a finite resource in one of the world’s most stable economies. Over a decade, the appreciation of a well-chosen terrace house often eclipses the initial tax outlay, transforming a high-cost entry into a high-value legacy.

Partnering with a Trusted Advocate

Executing a high-value transaction requires more than a standard agent; it demands a dedicated partner who understands the intersection of real estate and tax law. Vincent Lim provides a white-glove service level that coordinates seamlessly with your legal and tax professionals. This collaborative approach ensures that every detail, from valuation accuracy to remission applications, is handled with meticulous planning. Whether you are pursuing a sprawling GCB or a luxury condominium, you deserve a representative who values transparency and results above all else. This disciplined approach ensures your acquisition strategy is both legally sound and financially optimized.

Secure your financial future with a bespoke acquisition strategy. Contact Vincent Lim today to schedule a private wealth planning session and master your property progression.

Securing Your Generational Legacy in the 2026 Market

Success in Singapore’s luxury real estate market depends on your ability to transform tax liabilities into strategic advantages. We’ve detailed how residency profiles and property counts define your initial exposure, and how advanced mechanisms like decoupling and matrimonial remissions can protect your liquidity. When you view the abds for landed property as a manageable variable within a 10-year asset progression roadmap, you gain the clarity needed to secure high-value assets like detached houses or Good Class Bungalows with absolute confidence.

Navigating these high-stakes transactions requires a partner who operates with disciplined expertise. As a Strategic Partner at OrangeTee & Tie, Vincent Lim brings over 20 years of experience and a proven track record in complex GCB sales to your acquisition strategy. This seasoned authority ensures that every regulatory nuance is refined for your benefit, providing you with a white-glove service level that prioritizes transparency and results. It’s time to move beyond uncertainty and execute your vision with precision.

Refine your landed property strategy with Vincent Lim and take the first step toward a meticulously planned property portfolio. Your future legacy deserves nothing less than a gold-standard approach.

Frequently Asked Questions

What is the current ABSD rate for Singapore Citizens buying their second landed property?

Singapore Citizens pay a 20 percent ABSD rate when purchasing their second residential property. This rate is calculated based on the higher of the purchase price or the professional market valuation. It represents a significant step up from the 0 percent rate applied to an initial home purchase. You must ensure sufficient liquidity to manage this upfront cost, as it is a mandatory requirement for completing the transaction.

Can I use CPF to pay for the ABSD on a landed property?

You can use the savings in your CPF Ordinary Account (OA) to pay for the ABSD on a residential property. However, this usually functions as a reimbursement process if the stamp duty is due before the CPF funds can be released. For most private property transactions, you must first settle the tax in cash and then apply to have that amount reimbursed from your CPF account. It’s vital to verify your available OA balance before committing to the purchase.

Are foreigners allowed to buy landed property in Singapore, and what is their ABSD?

Foreigners are generally restricted from purchasing landed property and must obtain specific approval from the Land Dealings Approval Unit (LDAU). If granted permission, they are subject to a flat 60 percent ABSD rate on the purchase. This high barrier reflects the government’s strategy to prioritize land ownership for Singapore Citizens. Certain individuals from countries with specific Free Trade Agreements may be eligible for tax treatment equivalent to Singapore Citizens. For a full breakdown of the eligibility criteria and strategic pathways available, review the complete guide on whether foreigners can buy landed property in Singapore under the 2026 regulatory framework.

How does the ABSD (Trust) rule affect buying a house for my children?

Any residential property transferred into a living trust is subject to an upfront ABSD (Trust) rate of 65 percent. You may apply for a remission of this tax if the trust identifies a specific individual beneficiary and the property vests in them immediately. This regulation ensures that trusts are utilized for genuine legacy planning and wealth preservation for the next generation rather than as a mechanism to circumvent property count restrictions.

Is there a way to get an ABSD refund when upgrading from a condo to a terrace house?

Singapore Citizen couples can apply for a refund of the abds for landed property through matrimonial remission. You are required to pay the tax upfront when acquiring the terrace house and must sell your existing condominium within six months of the purchase date. This refund mechanism provides essential financial relief for families transitioning to a larger home, provided all specific IRAS conditions and timelines are strictly followed.

What happens if I miscalculate my property count when declaring for ABSD?

Miscalculating your property count can result in severe financial penalties and potential legal action from IRAS. The authority maintains precise records of all residential interests, including partial shares or properties held through trusts. Under-declaring your liability is a serious offense that can lead to a fine of up to four times the unpaid duty. You should conduct a comprehensive audit of your local and global holdings to ensure absolute accuracy in your declaration.

Do I have to pay ABSD if I inherit a landed property?

You are not required to pay ABSD when you inherit a landed property through a will or the laws of intestacy. Inheritance is generally exempt from stamp duty because it is not a voluntary purchase transaction. However, the inherited property will be included in your total property count for any future residential acquisitions. This could potentially increase the tax bracket for your next purchase, affecting your long-term asset progression strategy.

How long do I have to pay the ABSD after signing the Option to Purchase (OTP)?

You must settle the ABSD within 14 days of exercising the Option to Purchase if the document is signed within Singapore. If the document is executed overseas, the deadline is 30 days after the document is received in Singapore. Given the high valuations typical of landed estates, securing your funding well in advance is a critical component of a disciplined and successful acquisition process. A comprehensive capital allocation plan that addresses your landed property downpayment in Singapore alongside stamp duty obligations ensures you are fully prepared to meet these strict payment deadlines without compromising your broader financial strategy.