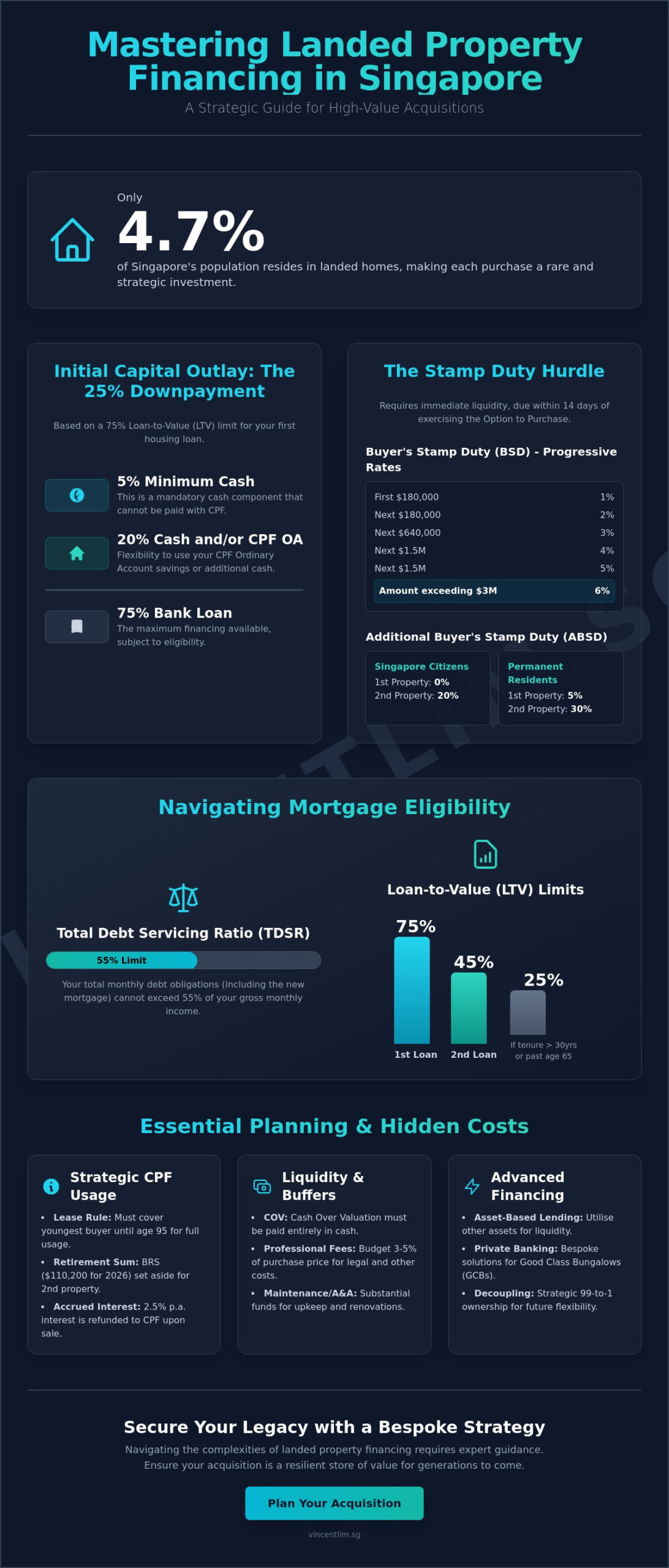

Did you know that only 4.7% of Singapore’s population resides in landed homes? This extreme scarcity transforms every acquisition into a sophisticated capital management exercise rather than a standard real estate transaction. You likely understand that securing such a prestigious asset requires more than just significant wealth. The current 55% TDSR threshold and the complexity of progressive stamp duties often create unexpected hurdles for even the most seasoned investors. It’s natural to feel concerned about how these regulatory limits might impact your borrowing power or long-term liquidity.

This guide provides the clarity you need to master the intricacies of financing a landed property purchase in singapore with absolute confidence. We’ll move beyond basic mortgage applications to explore strategic capital allocation and the impact of the 2026 CPF Basic Retirement Sum requirements. You’ll gain a structured framework for balancing cash reserves against CPF usage while accounting for the essential costs of property maintenance and potential additions. By the end of this article, you’ll have a refined plan to navigate the 75% LTV limit and secure your legacy in Singapore’s most exclusive residential tier.

Key Takeaways

- Define the initial capital requirements, including the mandatory 5% cash downpayment and progressive stamp duty obligations for high-value homes.

- Optimize your mortgage eligibility by understanding how the 55% TDSR threshold and 75% LTV limits impact your financing a landed property purchase in singapore.

- Learn how asset-based lending and private banking approaches can provide the liquidity needed for Good Class Bungalows and other elite assets.

- Account for the long-term financial commitments of landed ownership, including progressive property taxes and the substantial budgeting required for A&A works.

- Strategic selection between freehold and leasehold tenures ensures your acquisition remains a resilient store of value for future generations.

Calculating the Initial Outlay: Cash, CPF, and Stamp Duties

Securing a landed home in Singapore requires a meticulous approach to liquidity that differs significantly from the entry requirements of Singapore’s public housing system. While high-net-worth individuals often possess the necessary capital, the challenge lies in the strategic timing and allocation of these funds. A standard acquisition begins with the 25% downpayment rule. Under the current 75% Loan-to-Value (LTV) limit for a first housing loan, you must provide a minimum of 5% in cash. The remaining 20% can be settled using a combination of cash and your CPF Ordinary Account (OA) savings.

The financial commitment extends beyond the downpayment. In 2026, the Buyer’s Stamp Duty (BSD) remains a progressive tax that heavily impacts the luxury segment. For properties valued above $3 million, the portion exceeding this threshold is taxed at 6%. When financing a landed property purchase in singapore, you must also account for the Additional Buyer’s Stamp Duty (ABSD) if this is not your first residential asset. For Singapore Citizens, a second property carries a 20% ABSD, while Permanent Residents face a 5% levy on their first purchase and 30% on their second. These duties are typically due within 14 days of exercising the Option to Purchase, requiring immediate and substantial liquidity.

The Cash Upfront Component

Liquidity is the ultimate safeguard in the landed market. You must prepare for potential valuation gaps, often referred to as Cash Over Valuation (COV). If the purchase price exceeds the bank’s professional valuation, the difference must be paid entirely in cash as it cannot be covered by the home loan. Beyond the purchase price, you should set aside a buffer for professional fees. Legal fees for landed transactions are generally higher due to the complexity of title searches. Valuation reports and initial administrative costs also require ready cash. We recommend maintaining a reserve of at least 3% to 5% of the purchase price to cover these immediate post-purchase expenses without straining your primary capital pools.

Utilising CPF Savings Strategically

While CPF OA funds are a valuable resource for financing a landed property purchase in singapore, their use is governed by strict age and lease requirements. To utilize your full CPF entitlement, the property’s remaining lease must cover the youngest buyer until at least age 95. If the lease is shorter, the usable amount is pro-rated. If you are purchasing a second property, you must also set aside the 2026 Basic Retirement Sum of $110,200 before OA funds can be applied. You should also weigh the long-term impact of the 2.5% accrued interest, which must be refunded to your CPF account upon the eventual sale of the property. Balancing CPF for the initial downpayment versus preserving it for monthly installments is a decision that impacts your retirement liquidity years down the road.

Navigating Mortgage Eligibility: LTV Limits and TDSR in 2026

Understanding your borrowing capacity is the cornerstone of any successful high-value acquisition. Your first residential loan remains your most potent financial lever, offering a maximum Loan-to-Value (LTV) ratio of 75%. However, financing a landed property purchase in singapore becomes exponentially more complex if you already hold existing mortgages. The regulatory environment in 2026 demands a rigorous stress-test calculation, where banks apply a standardized interest rate to ensure you can withstand potential market fluctuations. Unlike public housing or Executive Condominiums, landed properties are exempt from the Mortgage Servicing Ratio (MSR). Instead, your eligibility is dictated by the Total Debt Servicing Ratio (TDSR) framework, which accounts for your entire debt portfolio.

LTV Ratios and Multiple Property Loans

The LTV limit experiences a steep drop for individuals with existing housing loans. If you’re carrying one outstanding mortgage, your maximum LTV for a new landed purchase falls to 45%, or even 25% if the loan tenure exceeds 30 years or extends past age 65. This significantly increases the cash outlay required. Many savvy investors utilize a tenancy-in-common structure, such as a 99-to-1 shareholding, to facilitate future decoupling strategies. By transferring shares later, one party can potentially “free up” their name to secure a higher LTV for a subsequent purchase. If you’re planning a multi-property portfolio, it’s wise to seek a bespoke financing assessment to align your ownership structure with your long-term leverage goals.

TDSR and Income Recognition

High-net-worth individuals (HNWIs) often face unique challenges during the credit assessment process. Banks typically apply a 30% “haircut” to variable income sources, such as performance bonuses, commissions, and rental income. This means only 70% of these earnings count toward your debt-servicing ability. TDSR is the 55% cap on gross monthly income for all debt repayments. Your existing obligations, including luxury car loans, credit lines, and personal loans, are all subtracted from this 55% limit. To maximize your loan quantum, it’s often strategic to clear smaller, high-interest debts before submitting your mortgage application. This ensures your financing a landed property purchase in singapore is supported by the highest possible eligible income profile.

Strategic Financing for High-Value Assets and GCBs

High-value acquisitions, specifically those exceeding the $20 million mark, often transcend the capabilities of standard retail banking. When you’re looking at what is a good class bungalow, the financing structure shifts from simple debt servicing to complex wealth management. Private banks and wealth management arms provide bespoke solutions that retail branches cannot match. This often involves asset-based lending, where your global investment portfolio, including stocks and bonds, is pledged as collateral to enhance your borrowing capacity. This approach is particularly effective for business owners who have substantial liquid assets but require flexibility in how they demonstrate income. It allows for a more holistic view of your net worth rather than relying solely on traditional monthly salary slips.

Financing for Good Class Bungalows (GCBs)

GCBs represent the pinnacle of the market, but their massive land plots present unique valuation challenges. Standard retail banks often struggle with the sheer loan quantums required for these multi-million dollar assets. Valuation discrepancies are common, as the value is often tied to the potential for redevelopment or the prestige of a specific enclave. Private banks address this by offering credit facilities tailored to the client’s total relationship value. These institutions are more adept at structuring loans that account for the 6% Buyer’s Stamp Duty (BSD) on the portion of the purchase price exceeding $3 million. They provide the agility needed to secure these rare assets before they’re snapped up by other elite buyers in a competitive market.

Bridging Loans and Asset Progression

Managing the transition between properties is a critical phase of capital allocation. If you’re upgrading from a condo to landed, you might encounter a temporary liquidity gap. Bridging loans serve as a short-term financial bridge, typically lasting six months, to cover the downpayment of your new home while you wait for the proceeds from your previous sale. While these are often interest-only loans, they require a disciplined exit strategy. Miscalculating the timeline can lead to significant interest costs or delays in ABSD remission applications. Financing a landed property purchase in singapore through a bridging loan requires precise coordination between your legal counsel and your private banker to ensure a seamless capital flow. This methodical planning ensures that your legacy remains secure throughout the transition without compromising your primary liquidity reserves.

The Hidden Costs: Maintenance, Taxes, and A&A Budgeting

Owning a landed home is a privilege that demands a disciplined approach to asset stewardship. While the initial capital outlay is often the primary focus, a robust strategy for financing a landed property purchase in singapore must incorporate the recurring financial obligations of ownership. Unlike the consolidated management fees found in luxury condominiums, the responsibility for a landed property’s structural integrity and regulatory compliance rests solely with you. This shift requires a mental transition from being a resident to acting as an active asset manager.

Regular maintenance is a strategic necessity. In our tropical environment, neglecting roof inspections or specialized pest control can lead to structural degradation that erodes your property’s market value. You should proactively budget for professional landscaping, pool filtration servicing, and facade preservation. High-value assets also require comprehensive insurance coverage that extends beyond basic fire protection. A bespoke policy should cover the full reinstatement cost of the property, protecting the unique architectural features and high-end finishes that define your home. It’s also prudent to include coverage for public liability and alternative accommodation expenses to ensure total peace of mind.

Addition & Alteration (A&A) Financing

Many buyers prioritize properties with the potential for customization. However, standard renovation loans are typically capped at $30,000, which is insufficient for the high-level modifications required in the landed segment. For significant works, you’ll need to explore construction loans or building loans that are integrated into your initial mortgage structure. A&A costs for a detached house for sale singapore can exceed $1M depending on the scope. When integrating these costs, lenders usually require detailed quotations from BCA-registered contractors to assess the “as-if-complete” valuation. This meticulous planning ensures your capital remains liquid enough to see the project through to completion without compromising your primary mortgage obligations.

Property Tax and Annual Value (AV)

Property tax in 2026 remains a significant annual commitment that scales with the prestige of your residence. The Inland Revenue Authority of Singapore (IRAS) determines your property’s Annual Value (AV) based on estimated market rentals of comparable homes in your area. For owner-occupied landed properties, the tax rates are progressive. While the first $12,000 of AV is exempt, the rates climb steadily, reaching 32% for the portion of AV exceeding $100,000. It’s common for landed owners to manage five-figure annual tax bills. If you’re considering an investment property that isn’t owner-occupied, these rates are even more substantial, starting at 12% for the first $30,000 of AV. Understanding these tiers is essential for accurate long-term cash flow modeling.

If you’re unsure how these hidden costs will affect your long-term capital allocation, it’s essential to consult with a dedicated real estate strategist who can provide a comprehensive financial simulation tailored to your specific acquisition goals.

Securing Your Legacy: Why a Bespoke Strategy Matters

A landed home in Singapore represents the ultimate expression of financial achievement and long-term stewardship. It isn’t merely a residence; it’s a multigenerational wealth vehicle that requires a financing strategy as sophisticated as the asset itself. When you’re financing a landed property purchase in singapore, you aren’t just looking at the next five years. You’re planning for a legacy that could span decades. This foresight ensures that your capital remains productive while your family enjoys the security of a tangible, high-value asset. Moving forward without a structured plan can lead to missed opportunities in a market where timing and precision are everything.

The first practical step in this journey is obtaining a formal In-Principle Approval (IPA). In the competitive 2026 landscape, a seller’s confidence is often tied to a buyer’s proven financial readiness. An IPA provides you with a definitive loan quantum, allowing you to negotiate from a position of strength and certainty. It eliminates the risk of an aborted transaction due to unforeseen Total Debt Servicing Ratio (TDSR) or valuation issues. By securing your financing framework early, you can focus your attention on selecting the right plot and architectural style that aligns with your family’s needs.

Freehold vs. Leasehold Value Retention

The choice between tenures is one of the most critical decisions affecting your long-term financing. Banks typically offer more favorable mortgage tenures for freehold terrace houses because they don’t face the “lease decay” that affects older leasehold properties. As a leasehold property ages, financing restrictions often tighten. For instance, if the remaining lease is less than 60 years, the Loan-to-Value (LTV) limit and CPF usage may be significantly reduced for future buyers. This directly impacts the property’s eventual resale value and liquidity. A freehold title, by contrast, provides a stable foundation for legacy planning, ensuring that the asset remains a powerful store of value for the next generation.

The Vincent Lim Advantage

Navigating the complexities of high-value real estate requires more than just a standard agent; it demands the expertise of a seasoned landed property specialist. With over 20 years of experience in Singapore’s luxury market, Vincent Lim provides a bespoke advisory service that looks at your entire real estate portfolio. He coordinates the essential ecosystem of bankers, lawyers, and professional valuers to ensure every aspect of your acquisition is handled with meticulous care. This white-glove approach minimizes the stress of financing a landed property purchase in singapore, allowing you to transition into your new home with absolute confidence. From initial capital allocation to the final handover, you’ll have a dedicated advocate who values integrity and excellence as much as you do.

Refining Your Capital Strategy for a Seamless Acquisition

Mastering the intricacies of the landed market requires more than just capital; it demands a calculated approach to leverage and liquidity. You’ve explored how the 55% TDSR threshold and progressive stamp duties define your entry point, while long-term costs like A&A works and property taxes shape your ongoing commitment. Successfully financing a landed property purchase in singapore is about aligning these regulatory requirements with your personal wealth goals to ensure a resilient legacy for your family.

Navigating this high-stakes environment is simpler when you have a veteran strategist by your side. As an Executive Associate Director at OrangeTee & Tie, I’ve specialized in the GCB and luxury landed segments since 2004. My bespoke advisory service combines deep industry knowledge with a proven track record in high-value asset progression to provide you with absolute clarity and peace of mind. It’s about more than just a transaction; it’s about acting as a high-level partner in your success.

Ready to refine your capital allocation and secure your next home? Consult Vincent Lim for a Bespoke Landed Financing Strategy today. Your journey toward a successful landed acquisition deserves a partner who values precision and transparency as much as you do.

Frequently Asked Questions

How much cash downpayment is needed for a $5 million landed house?

For a $5 million landed home, you require a minimum cash downpayment of $250,000, which represents 5% of the purchase price. The subsequent 20% ($1 million) can be settled using either cash or your CPF Ordinary Account savings, provided you qualify for the maximum 75% LTV. It’s vital to account for potential valuation gaps, as any price paid above the bank’s professional valuation must be covered entirely in cash.

Can I use my CPF to pay for the Buyer’s Stamp Duty on a landed property?

Yes, you can utilize your CPF Ordinary Account savings to pay for the Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD). However, because these duties are due within 14 days of exercising the Option to Purchase, buyers often pay in cash first and later seek reimbursement from their CPF funds. This ensures you meet the strict IRAS deadlines while preserving your liquid cash reserves for other immediate acquisition costs.

What is the current TDSR limit for property loans in Singapore for 2026?

The Total Debt Servicing Ratio (TDSR) threshold for 2026 is maintained at 55% of your gross monthly income. This means your total monthly debt obligations, including the new mortgage, car loans, and credit card balances, cannot exceed this limit. When financing a landed property purchase in singapore, banks apply a medium-term interest rate stress test to your application to ensure financial resilience against future market fluctuations.

Is it harder to get a loan for a leasehold landed property than a freehold one?

While it isn’t necessarily harder to obtain a loan for leasehold properties, banks apply stricter criteria as the lease decays. If a property has less than 60 years remaining, the loan tenure and LTV limit may be reduced. Freehold properties are generally preferred by lenders for long-term financing because they don’t face leasehold depreciation, making them more stable collateral for high-value mortgages and multigenerational legacy planning.

How does an In-Principle Approval (IPA) help in the landed property search?

An In-Principle Approval (IPA) acts as a definitive confirmation of your borrowing capacity, allowing you to search with absolute certainty. In the competitive landed segment, having an IPA in hand signals to sellers that you’re a serious, qualified buyer. This often provides a significant advantage during price negotiations, as it minimizes the risk of the deal falling through due to a rejected mortgage application or an unexpected valuation shortfall.

Can a foreigner get a mortgage for a landed property purchase in Singapore?

Foreigners are generally restricted from purchasing landed property on mainland Singapore and must obtain approval from the Land Dealings Approval Unit (LDAU). If granted, or if purchasing in Sentosa Cove, they can obtain a mortgage. However, they must navigate a 60% ABSD and the standard 75% LTV limit. Most international buyers find that financing a landed property purchase in singapore requires substantial liquid capital to manage these high entry costs.

What happens to my LTV if I already have an existing condo loan?

If you hold an existing mortgage for a condominium, your LTV for a second residential property drops significantly to 45%. This limit can decrease further to 25% if the loan tenure exceeds 30 years or extends past the age of 65. This regulatory framework is designed to prevent over-leveraging, requiring you to provide a much larger cash and CPF component to secure your landed acquisition compared to your first property purchase.

Are there specific grants available for first-time landed property buyers?

There are currently no government grants available for the purchase of private landed property in Singapore. Central Provident Fund (CPF) housing grants are exclusively reserved for eligible buyers of HDB flats or new Executive Condominiums. Landed property acquisitions are viewed as high-net-worth investments, where buyers are expected to rely on their personal capital, CPF Ordinary Account savings, and private bank financing to complete the transaction without state subsidies.