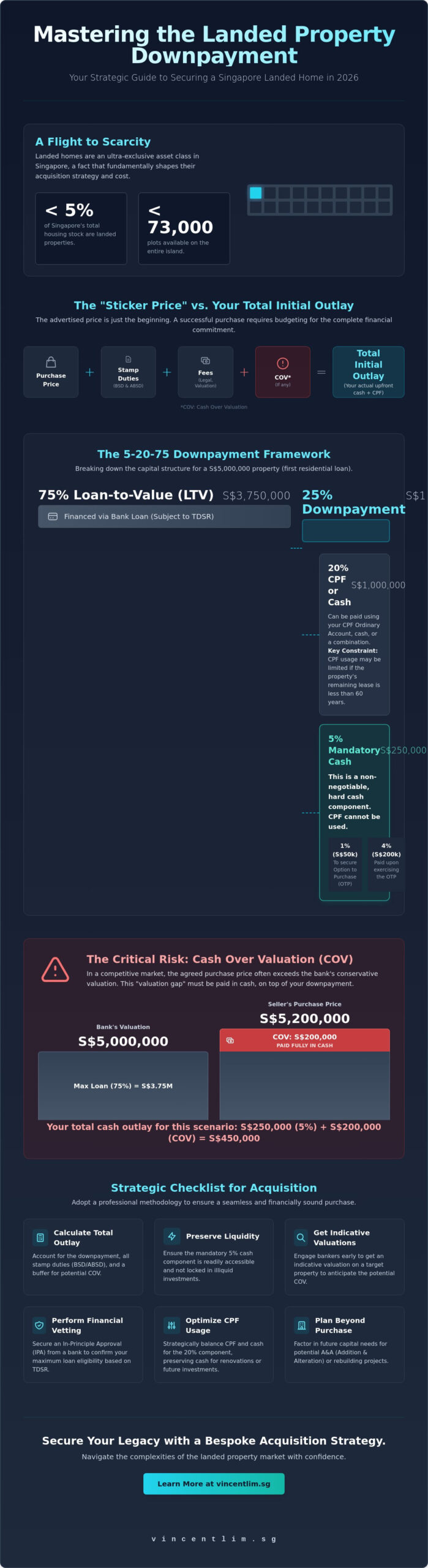

With fewer than 73,000 plots remaining, landed homes represent less than 5% of Singapore’s total housing stock, a scarcity that has pushed entry-level inter-terrace prices toward the S$5 million mark in 2026. For the discerning buyer, the primary challenge isn’t merely finding the right address; it’s the complex orchestration of a landed property downpayment singapore. You likely recognize that a standard 25% outlay is only the starting point of a much deeper financial commitment in a market where valuation gaps can fluctuate overnight.

We understand the anxiety that stems from unpredictable bank valuations and the evolving 2026 ABSD landscape for multi-property portfolios. This guide serves as your strategic roadmap, offering the precision required to manage LTV limits and “Cash Over Valuation” risks with total confidence. You’ll gain a clear understanding of how to structure your initial 5% cash and 20% CPF components while optimizing capital for future A&A or rebuilding projects. This analysis provides the financial certainty you need to secure your place in Singapore’s most prestigious asset class without over-leveraging your position.

Key Takeaways

- Learn to calculate the true “Total Initial Outlay” by accounting for progressive taxes and valuation discrepancies that extend beyond the advertised purchase price.

- Master the 5-20-75 framework to strategically manage your landed property downpayment singapore while preserving liquidity for the mandatory 5% cash component.

- Discover how to navigate the “Valuation Gap” to ensure you’re prepared for Cash Over Valuation (COV) scenarios where bank assessments lag behind market rates.

- Understand the impact of the 2026 ABSD and BSD regulations on your upfront capital to avoid common pitfalls in multi-property portfolio expansion.

- Adopt a professional methodology for financial vetting and indicative valuations to ensure a seamless transition into the landed asset class.

Navigating the Financial Landscape of Landed Property Entry Costs in 2026

Transitioning from a luxury condominium to a landed home is a significant milestone, but the financial transition involves more than just a higher price tag. In Singapore’s housing landscape, landed assets operate on different mathematical principles than strata-titled developments. While a condominium offers shared ownership of common facilities, a landed property represents fee-simple land ownership, a distinction that fundamentally alters your landed property downpayment singapore strategy. Every plot is unique, and this individuality means you can’t rely on the “last transacted price” of a neighbor to guarantee your own bank valuation.

Understanding the “Sticker Price” vs. Total Initial Outlay

The advertised price of a terrace house or bungalow is only the first layer of capital. Beyond the purchase price, you’ll encounter professional fees and administrative costs that are significantly higher than those in the condo market. These include specialized valuation reports and more extensive legal fees for complex title searches. Total Initial Outlay is the sum of the downpayment, stamp duties, and valuation gaps. Failing to account for these “hidden” layers can lead to a liquidity crunch right at the point of purchase.

Why 2026 Market Dynamics Demand Greater Upfront Liquidity

The 2026 market is defined by a “flight to scarcity.” With only 73,000 landed plots available, competition drives a wedge between bank valuations and transaction prices. When evaluating freehold vs leasehold landed property, remember that banks maintain conservative Loan-to-Value (LTV) limits for landed homes. If a bank’s valuation lags behind the seller’s asking price, you’re expected to cover that difference entirely in cash. This “Cash Over Valuation” (COV) directly inflates your landed property downpayment singapore beyond the standard 25%.

Current interest rate environments also play a role. While rates have stabilized, borrowing capacity remains tightly regulated by the Total Debt Servicing Ratio (TDSR). Because landed properties command higher absolute prices, even a slight shift in interest rates can significantly impact your eligibility. This is why a seasoned specialist must vet your financial position before you even begin viewing properties. It ensures that your time is spent on acquisitions that are both prestigious and financially viable.

The 5-20-75 Framework: Breaking Down Your Downpayment Components

Mastering the landed property downpayment singapore requires a granular understanding of how capital is partitioned during the acquisition phase. For most buyers securing their first residential loan, the framework follows a 5-20-75 structure. This represents the 5% mandatory cash component, the 20% CPF or cash portion, and the 75% Loan-to-Value (LTV) ceiling. While this sounds straightforward, the execution demands meticulous timing and a clear view of your liquid reserves.

The 5% Mandatory Cash Component: Non-Negotiable Liquidity

The first 5% of the purchase price is the most critical hurdle in the initial timeline. This amount is typically split between the 1% required to secure the Option to Purchase (OTP) and the remaining 4% paid when you exercise that option. You must pay this entirely in “hard cash” because CPF funds cannot be used for the initial booking or option fees. Banks and legal firms require these funds to be cleared within a tight 14-to-21-day window. If your capital is locked in fixed deposits or equity markets, you’ll need to orchestrate the liquidation well before signing any legal documents to avoid a breach of contract.

Optimizing Your CPF OA for the 20% Component

The subsequent 20% of your landed property downpayment singapore offers more flexibility, as it can be settled using your CPF Ordinary Account (OA), cash, or a combination of both. However, older landed properties introduce specific constraints. If the property’s remaining lease is less than 60 years, the amount of CPF you can use is pro-rated based on the youngest buyer’s age. If the lease is too short, you might face a “CPF Withdrawal Limit” that forces a higher cash outlay than originally planned. Balancing your CPF usage is a strategic choice; using cash preserves your OA for a stable 2.5% return, while using CPF maximizes your immediate liquidity for potential renovations.

Navigating LTV Limits for First and Subsequent Properties

The 75% LTV limit is the maximum leverage allowed under current MAS housing loan rules, provided you have no other outstanding housing loans. If you’re expanding a multi-property portfolio, the math shifts dramatically. A second loan requires a 50% downpayment, with 25% mandatory in cash. Furthermore, if the loan tenure exceeds 30 years or extends past the borrower’s age of 65, the LTV drops even further. To ensure you aren’t caught in an LTV trap, it’s wise to consult a specialist who can run indicative stress tests on your borrowing capacity before you commit to a high-value acquisition.

Overcoming the Valuation Gap: The Critical Factor in High-Value Acquisitions

A common misconception among high-net-worth buyers is that the 25% landed property downpayment singapore is always calculated against the agreed purchase price. In reality, financial institutions apply the Loan-to-Value (LTV) limit to the lower of the purchase price or the professional bank valuation. This discrepancy creates the “Valuation Gap,” a financial void that you must bridge entirely with cash. In a market where scarcity drives prices upward faster than conservative bank algorithms can adjust, understanding this gap is the difference between a successful acquisition and a failed transaction.

Why Bank Valuations Lag in the Landed Segment

Unlike luxury condominiums where dozens of identical “cookie-cutter” units provide clear price benchmarks, landed properties are heterogeneous. Each plot possesses unique attributes such as frontage width, plot shape, and terrain elevation that significantly influence market value but are often undervalued by desk-bound bank appraisers. Banks typically adopt a conservative stance, especially on older, non-renovated homes where the value lies primarily in the land. Even when record-breaking transactions occur in the Good Class Bungalow segment, these new price floors take months to reflect in official bank valuations. This lag is a byproduct of the MAS Financing Rules for Residential Property, which encourage prudent lending based on historical data rather than speculative future growth.

Calculating Your Real Cash Requirement including COV

To determine your actual landed property downpayment singapore, you must factor in the Cash Over Valuation (COV). The formula is: (Purchase Price – Bank Valuation) + (25% of Bank Valuation). Let’s analyze a scenario involving a S$5 million terrace house. If the bank values the property at only S$4.8 million, your 75% loan is capped at S$3.6 million. Your total upfront capital requirement would be:

- The Valuation Gap (COV): S$200,000 (Paid in Cash)

- Mandatory 5% Cash Component: S$240,000 (5% of S$4.8M)

- Remaining 20% Downpayment: S$960,000 (CPF or Cash)

- Total Initial Outlay: S$1,400,000

In this example, the actual “downpayment” isn’t 25% of the sticker price; it’s effectively 28% of the total cost. Without pre-planned liquidity, a S$200,000 valuation shortfall can derail an acquisition after the Option to Purchase (OTP) has been signed. To mitigate this risk, seasoned strategists always secure multiple “indicative valuations” from different lenders before committing to a price. This proactive vetting ensures that your capital allocation remains optimized and your transition into the landed asset class stays seamless.

Strategic Liquidity Planning: Beyond the Initial 25%

Securing the 25% landed property downpayment singapore is a significant milestone, yet it represents only the first phase of a sophisticated capital allocation strategy. For elite acquisitions, the true “entry cost” often exceeds the sticker price by a considerable margin. A strategist must account for progressive tax structures and professional fees that require immediate liquidity. Failing to plan for these secondary outlays can compromise your ability to enhance the property’s value through future redevelopment or sophisticated architectural interventions.

Budgeting for BSD and ABSD for Landed Property

Buyer’s Stamp Duty (BSD) is a progressive tax that becomes increasingly significant as property values climb. For residential assets priced above S$3 million, the top marginal rate is 6%. On a S$10 million detached house, the BSD alone exceeds S$500,000. This amount must be paid within 14 days of exercising the Option to Purchase (OTP). If you’re acquiring a second residential property, the Additional Buyer’s Stamp Duty (ABSD) adds another 20% for Singapore Citizens. The financial landscape is even more demanding for foreigners/PRs, who face higher ABSD tiers that must be settled in cash upfront. These taxes are not just administrative hurdles; they’re substantial capital commitments that influence your overall leverage.

Factoring in A&A or Full Rebuild Reserves

In the landed segment, value is often concentrated in the land rather than the existing structure. Many investors acquire older terrace or semi-detached houses with the specific intent of a full rebuild or significant Addition & Alteration (A&A) works. A comprehensive reconstruction can easily command a budget of S$1 million or more. While construction loans are available, they operate differently from standard mortgage products, often requiring you to fund the initial stages of work before disbursements begin. It’s vital to ensure your landed property downpayment singapore doesn’t exhaust the “improvement capital” needed to transform a legacy plot into a modern masterpiece. Preserving this liquidity allows you to maintain momentum during the design and construction phases.

Beyond construction, your roadmap should include provisions for legal fees and specialized valuation reports. These professional services ensure that the title is clear and the land size is accurately reflected. A disciplined approach to these costs provides the peace of mind that your investment is protected from the outset. If you’re ready to refine your capital plan for a high-stakes acquisition, you can explore bespoke landed property strategies that align with your long-term wealth objectives.

Securing Your Legacy with a Bespoke Landed Acquisition Strategy

Acquiring a landed home in Singapore is a sophisticated exercise in capital deployment that transcends the mechanics of a standard real estate transaction. While a typical agent focuses on the immediate sale, an elite strategist views your landed property downpayment singapore as a foundational move in a much larger wealth narrative. This approach requires a synthesis of market intelligence, financial precision, and long-term vision. It ensures that every dollar allocated today serves your family’s interests for generations to come.

The Role of an Elite Strategist in Financial Vetting

Success in the landed market begins long before the first viewing. Vincent Lim’s methodology centers on rigorous financial vetting to pre-empt hurdles like the Total Debt Servicing Ratio (TDSR). By analyzing your portfolio upfront, we identify potential borrowing constraints that could jeopardize a high-stakes deal. We don’t just wait for bank valuations to arrive; we actively coordinate with a network of specialized bankers to secure indicative valuations and the most favorable LTV structures. This proactive coordination is especially vital when exploring off-market opportunities, where realistic valuation expectations are the key to securing rare plots before they reach the public eye.

Transitioning from Transaction to Asset Progression

Your landed property downpayment singapore is the gateway to a prestigious asset class that offers unparalleled scarcity and privacy. However, the journey shouldn’t end at the point of handover. True asset progression involves structuring ownership for maximum tax efficiency and protection against future regulatory shifts. Whether you’re moving from a luxury condominium to a terrace house or eyeing a Good Class Bungalow, the strategy must account for your family’s evolving needs. We help you look past the immediate costs to see the property as a multi-generational legacy, ensuring your capital is positioned for both stability and appreciation.

Working with a veteran specialist like Vincent Lim provides the reassurance that your acquisition is handled with the highest level of discipline and transparency. We translate complex technical requirements into a clear, actionable roadmap, allowing you to move with the confidence of a seasoned investor. If you’re ready to refine your acquisition strategy and secure a premier landed asset, the first step is a confidential review of your financial portfolio. This ensures your transition into Singapore’s most exclusive residential segment is as seamless as it is rewarding.

Mastering Your Entry into Singapore’s Elite Residential Market

Navigating the complexities of a landed property downpayment singapore requires more than just liquid capital; it demands a surgical approach to valuation gaps and tax optimization. You now understand that the 5-20-75 framework is merely the baseline. True success lies in accounting for Cash Over Valuation and the progressive 2026 stamp duty landscape. By prioritizing indicative valuations and liquidity for potential redevelopment, you’ll position yourself to secure an asset that serves as a cornerstone for your family’s future.

Precision in these high-stakes transactions is non-negotiable. As an Executive Associate Director at OrangeTee & Tie and a specialist in GCB and luxury landed sales since 2004, Vincent Lim provides the seasoned expertise required to navigate these financial nuances. You can consult Vincent Lim for a bespoke landed financial strategy to ensure your asset progression and legacy planning are executed with absolute certainty. Moving into Singapore’s most prestigious housing segment is a significant achievement. With the right strategic partner, your transition will be both seamless and rewarding.

Frequently Asked Questions

Can I use CPF to pay for the 5% cash component of a landed property?

No, you cannot use CPF for the initial 5% cash component. This portion must be paid in hard cash during the Option to Purchase (OTP) and exercise stages. Your CPF Ordinary Account funds are only applicable for the remaining 20% of the landed property downpayment singapore and the associated Buyer’s Stamp Duty. Ensuring you have this liquidity ready is a fundamental step in the acquisition process.

How much is the typical valuation gap for a semi-detached house in 2026?

Valuation gaps for semi-detached houses in 2026 frequently range between 3% and 8% of the purchase price. This discrepancy arises because market demand for scarce plots often outpaces the conservative historical data used by bank appraisers. Because every landed property is unique; these gaps are more pronounced than in the condominium segment. You should prepare a cash reserve specifically to bridge this potential shortfall.

What happens if the bank valuation is lower than my purchase price?

If the bank valuation is lower than the purchase price, you must cover the entire difference in cash. This is known as Cash Over Valuation (COV). The bank will only lend up to 75% of the lower figure. For example, on a S$5 million purchase with a S$4.8 million valuation, the loan is capped at S$3.6 million, requiring you to fund the S$200,000 gap out of pocket.

Are there different downpayment rules for Good Class Bungalows (GCBs)?

The 5-20-75 framework remains the standard for Good Class Bungalows, but the absolute capital requirement is significantly higher. Since GCBs typically start at S$20 million, the 5% cash component alone requires S$1 million in immediate liquidity. Additionally, GCB buyers must be Singapore Citizens. The scale of these transactions means that even a small valuation gap requires substantial cash reserves to close the deal.

How does the Total Debt Servicing Ratio (TDSR) affect my landed property loan amount?

The Total Debt Servicing Ratio limits your total monthly debt obligations to 55% of your gross monthly income. This regulation directly impacts your landed property downpayment singapore strategy because it may prevent you from reaching the maximum 75% loan-to-value limit. If your income doesn’t support the loan amount for a high-value landed home, you’ll need to increase your upfront cash or CPF contribution to lower the loan quantum.

Can I take a renovation loan on top of my landed property mortgage?

You can take a renovation loan, but the capped amount, often around S$30,000, is usually insufficient for landed properties. Most owners opt for a construction loan or an Addition & Alteration (A&A) loan instead. These facilities are specifically designed for more extensive works and are disbursed in stages as the construction progresses. It’s a more strategic way to manage capital for large-scale improvements.

Do I need to pay ABSD upfront if I am selling my current condo to buy a landed home?

Yes, you must pay the Additional Buyer’s Stamp Duty (ABSD) upfront if your current condominium is not legally sold before you exercise the option for the landed home. As a Singapore Citizen, you’ll pay the 20% second-property rate. However, you’re eligible to apply for an ABSD remission if you sell your first property within six months of the landed property’s purchase date.

How long does it take to secure a bank valuation for a landed property?

Securing an indicative or desktop valuation typically takes between 2 to 3 business days. A formal, full valuation report involves a site visit and may take up to a week. Because landed homes have no identical comparables, banks require this time to assess the land’s specific attributes. It’s prudent to initiate this process early to avoid delays during the tight Option to Purchase window.